Cornerstone 2nd Quarter 2023 Commentary

August 4, 2023

“Life can only be understood backwards, but it must be lived forwards.” – Soren Kierkegaard

“There are two kinds of people who lose money: those who know nothing and those who know everything.” – Henry Kaufman (German-American economist) to Robert Lenzner in Forbes 10-19-1998 who added, “With two Nobel Prize winners in the house, Long-Term Capital clearly fits the second case.”

“Economics is a very difficult subject. I’ve compared it to trying to learn how to repair a car when the engine is running.” – Ben Bernanke

Sometimes looking in the rearview mirror is a smart choice! Nobel Prize winners are not always right, and neither are economists. Perhaps today with the most predicted recession in recent memory not materializing as anticipated, we would do well to remember that even brilliant strategists, economists, and Fed Chairmen can be wrong. That’s not to say that the recession isn’t coming. In fact, we think that it is, but it certainly hasn’t materialized yet.

“Yet” may be the key word in that phrase. Someone, perhaps Warren Buffet, suggested that markets can continue being irrational longer than we can remain solvent! Despite recessionary fears, the second quarter of 2023 witnessed a continuation of the rally begun in the fourth quarter of 2022. The bank failures of the first quarter were not sufficient to derail it.

Ten consecutive rate hikes by the U.S. Federal Reserve followed by an 11th hike this month have barely dented investor enthusiasm. When it comes to climbing the proverbial “wall of worry,” this market and this economy seem to be doing just fine. Still, the mini-banking crisis was enough to put a crimp in the positive performance of value-driven strategies. In the second quarter, euphoric predictions regarding our AI-driven future were enough to propel the technology sector to even more lofty heights. While the market rallied throughout the quarter, volatility fell further, confounding those prognosticators who view the future as something less than benign.

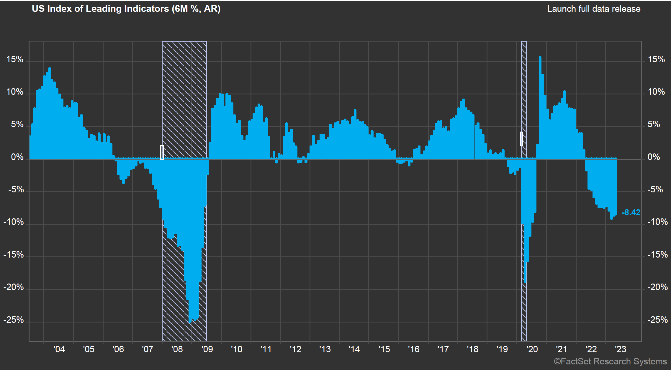

On the surface, it was a great quarter for stocks, and only mildly problematic from a bond perspective. Given the hawkishness of most central banks around the globe, bond performance through the first half of 2023 continues to hold up just fine. Despite continued contraction in the manufacturing sector, declines in leading economic indicators, and a persistently inverted yield curve, the U.S. economy continues to hold it together and exceed the growth expectations of virtually everyone! Perhaps this is one of those rare times when the market and the economy’s correlation is in sync and the collective wisdom of investors trumps that of the experts, but then again perhaps not. As we noted at the outset, “Life can only be understood backwards, but it must be lived forwards.”

Throughout most of the quarter the market narrowed, and by the end of June seven stocks accounted for approximately 73% of the first half gains of the S&P 500! The so called “Magnificent Seven,” comprising Apple, Microsoft, Alphabet (Google), Amazon, Meta Platforms (Facebook), Nvidia, and Tesla, drove the market higher throughout the second quarter as investors snapped up tech names linked to both the present and future of AI. In fact, the surge in these names ultimately resulted in the rebalancing of the NASDAQ Index, not too surprising when you consider that Apple’s market cap of $3 trillion is larger than most other stock markets around the world!

ull market. Rather the best we can hope for is a range-bound market with little upside and significant downside. In our mind the probability of recession continues to rise; it is only the question of timing that remains opaque. Consequently, we remain defensively postured as we enter the second quarter of 2023.

The S&P 500 ended the quarter up nearly 17% for the year. However, its equal weighted counterpart (S&P 500 Equal Weight) was only up 7% over the same period. This is indicative not only of the stratospheric valuations of the Magnificent Seven, but also the more modest value of the “Frugal 493” as Jack Hough referred to them in Barron’s Magazine a week or so ago. While the Magnificent Seven sport multiples in excess of 40x earnings, the remainder of the S&P 500 sports an average P/E of only 15, hardly stratospheric. While the rising tide of tech lifted all boats, the broader market was generally left in the dust. The Dow was up 4% in the quarter, but only 5% on a year-to-date basis. On a relative basis, this made for a tough first half for many equity portfolios!

Smaller cap stocks turned in a good quarter, but continue to trail their large cap brethren. The Russell 2000 was up over 5% for the quarter, bringing its year-to-date performance to positive 8%. Certainly, a strong first half showing, but the Index is trailing the S&P 500 by approximately 9 percentage points, and the Russell 1000 Growth, by over 20 percentage points. The value effect was a drag in small cap as well. The Russell 2000 Growth Index gained 7% during the second quarter while the Russell 2000 Value Index was only up 3%. In most quarters, one would be thrilled with a 3% return! REITs rallied as well up over 1% for the quarter and 2.97% on a year-to-date basis.

The growth factor was not quite as significant in overseas markets. The MSCI EAFE was up approximately 3% for the quarter and 12% on a year-to-date basis. Emerging markets stocks also moved up but now trail their developed market peers by a significant margin. The MSCI EM Index gained approximately 1% during the quarter but is up only 4.89% for the year. A weakening dollar has continued to provide some support for U.S. investors in international equities.

Finally, the bond market faded a bit in the face of continue Fed rate hikes, but overall returns for the first half were reasonable. The U.S. Bloomberg Aggregate Bond Index was down about 0.84% for the quarter but up over 2% for the first half. Yields remain strong, and even with a couple of additional Fed rate hikes, traditional investment grade fixed income should end the year with a solid positive return. The continued strength in the economy and general “risk on” theme of the second quarter led to strong performance in the high yield sector of the bond market as well, and the Bloomberg High Yield Index is up nearly 5.4% for the year.

So what can we say? The second quarter of 2023 certainly surpassed our expectations, and Wall Street strategists are changing their economic forecasts more frequently than Kim Kardashian changes outfits. In short, everyone is more optimistic, and the “soft landing” unicorn seems destined to appear.

Color us cautious…it is easy to get caught up in the fear of missing out. It is equally easy to abandon a consistent plan or well-constructed strategy to chase short-term returns. Markets do go up 70% of the time, so optimism is a required characteristic of the long-term investor, but so, we believe, is caution. Remember the phrase so often repeated in the press today? “Monetary Policy impacts the economy with Long and Variable Lags.” We might also add, “Trees don’t grow to the sky!” The yield curve remains inverted, and significant challenges remain ahead for the U.S. economy.

In our view, unemployment, fiscal policy largesse, and excess savings are the keys necessary to unlock the probable timing of a U.S. recession. Unemployment is generally a lagging indicator, and by the time it begins to trend up, the economy has already slowed significantly. Currently, the unemployment rate remains low, and the job market appears to be healthy. With consumers working and wages growing, it is difficult to see a recession on the immediate horizon. The Biden administration’s infra-structure spending hidden in the “Inflation Reduction Act” continues to stimulate economic development, support infrastructure spending, and help forestall a possible recession as well. Finally, the excess savings accumulated by consumers during COVID remain significant. Studies vary, but the $700-800 billion in excess savings may be enough to sustain consumer spending and push the possible recession into 2024, and perhaps indefinitely, resulting in a soft landing akin the one seen in 1994-95.

As we noted earlier, the broader part of the market has only recently begun to participate more fully in the 2023 rally. Therefore, it is possible that overall market appreciation could stall as tech declines and the average stock gains ground in the second half of the year. We believe this remains the most probable outcome. Consequently, we have retained our more defensive positioning with an overweight to more value-oriented strategies.

Many economic indicators including the yield curve continue to point toward a recession, and it is rare indeed that the markets rally significantly in the face of high valuation. Generally, either a period of consolidation or a decline is required to support longer term growth. With the Fed retaining a more hawkish stance, a war in Europe, higher than average market valuations, and a manufacturing contraction, caution seems warranted. The long-term strategic allocation discipline employed in our portfolios will allow us to participate in any unanticipated market advance while the defensive nature of our tactical positioning should help protect portfolios in the event that the “soft landing unicorn” proves elusive.